Note

Go to the end to download the full example code.

Time series forecasting#

This tutorial shows how to do zero-shot univariate forecasting with

tabicl.TabICLForecaster.

Make sure the forecast dependencies are installed:

pip install tabicl[forecast]

Time series forecasting as tabular regression#

tabicl.TabICLForecaster is inspired by

TabPFN-TS.

The forecaster wraps tabicl.TabICLRegressor and turns forecasting

into a tabular regression problem:

each row is one timestamp,

the target column is the series value,

time-aware features are added automatically (index, calendar, seasonality).

Note

Compared with tabicl.TabICLClassifier and

tabicl.TabICLRegressor, the forecasting interface is newer and has

not yet been evaluated on a large public benchmark. We may later provide

evaluations and enhancements for time series forecasting.

import numpy as np

import pandas as pd

from tabicl import TabICLForecaster

from tabicl.forecast import plot_forecast

Build a synthetic univariate series#

We create a daily series that mixes a linear trend, a weekly seasonality, an annual seasonality, and Gaussian noise.

This makes the task intuitive: the model should extrapolate trend and recurring patterns into the future.

rng = np.random.default_rng(0)

n_timesteps = 365 * 2 # two years of daily observations

dates = pd.date_range(start="2022-01-01", periods=n_timesteps, freq="D")

t = np.arange(n_timesteps)

trend = 0.05 * t

weekly_season = 5.0 * np.sin(2 * np.pi * t / 7)

annual_season = 10.0 * np.sin(2 * np.pi * t / 365)

noise = rng.normal(scale=1.5, size=n_timesteps)

target = trend + weekly_season + annual_season + noise

# For a single time series, ``timestamp`` and ``target`` are sufficient.

df = pd.DataFrame({"timestamp": dates, "target": target})

df.head()

This DataFrame follows the input format required by

tabicl.TabICLForecaster.predict_df():

required columns:

timestamp,targetoptional column:

item_id(for multiple series)use

prediction_lengthfor regular horizons, orfuture_dfwhen you already know future timestamps/covariates

Define forecast horizon and hold-out period#

We keep the last prediction_length points as a pseudo-future set.

context_dfis the observed history provided to the forecaster.test_dfis only used for visual comparison.

prediction_length = 30

context_df = df.iloc[:-prediction_length]

test_df = df.iloc[-prediction_length:]

Forecast with TabICLForecaster#

tabicl.TabICLForecaster.predict_df() returns one row per future

timestamp, with a point forecast and quantile columns for uncertainty.

forecaster = TabICLForecaster()

pred_df = forecaster.predict_df(context_df, prediction_length=prediction_length)

Predicting time series: 0%| | 0/1 [00:00<?, ?it/s]

Predicting time series: 100%|██████████| 1/1 [00:05<00:00, 5.89s/it]

Predicting time series: 100%|██████████| 1/1 [00:05<00:00, 5.89s/it]

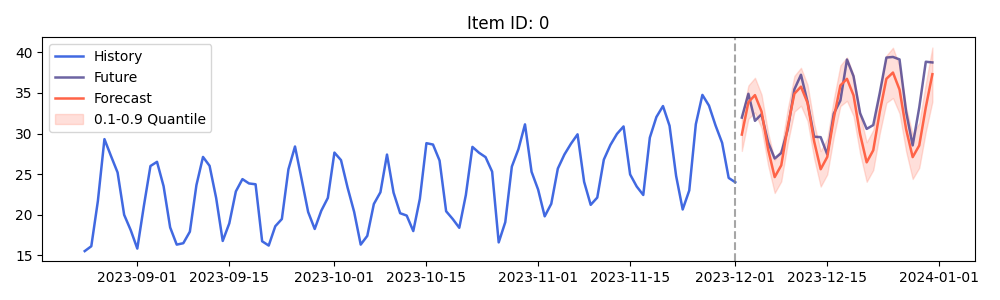

Plot context, forecast, and held-out truth#

fig, axes = plot_forecast(context_df=context_df, pred_df=pred_df, test_df=test_df)

A good forecast should continue the upward trend and recover the recurring

seasonal pattern visible in the held-out future values, which the

TabICLForecaster does successfully in this example.

Total running time of the script: (0 minutes 6.678 seconds)